Industrial circles frequently characterize Northern Mexico as a manufacturing engine. By 2030, the region is poised to become the primary testing ground for hydrogen-powered freight corridors, bridging the gap between Mexico’s industrial heartlands and the critical consumer markets of Texas and California. Global hydrogen growth is no longer the variable in question. The question is where early infrastructure will concentrate and why.

Hydrogen fueling stations do not appear randomly across a map. They cluster where truck volumes are dense, trade value is high, and policy funding is already flowing. If Mexico adds only a limited number of heavy-duty hydrogen refueling stations this decade, placement will determine whether the network becomes symbolic or strategic.

This article maps the likely nodes, the freight math behind them, and the infrastructure signals that could turn early pilots into durable cross-border corridors.

Mexico Hydrogen Fueling Station Market Analysis: Forecasts and Regional Growth Metrics

Analyzing current economic indicators reveals a significant growth trajectory for clean energy infrastructure along the northern border. The following data points outline the projected expansion:

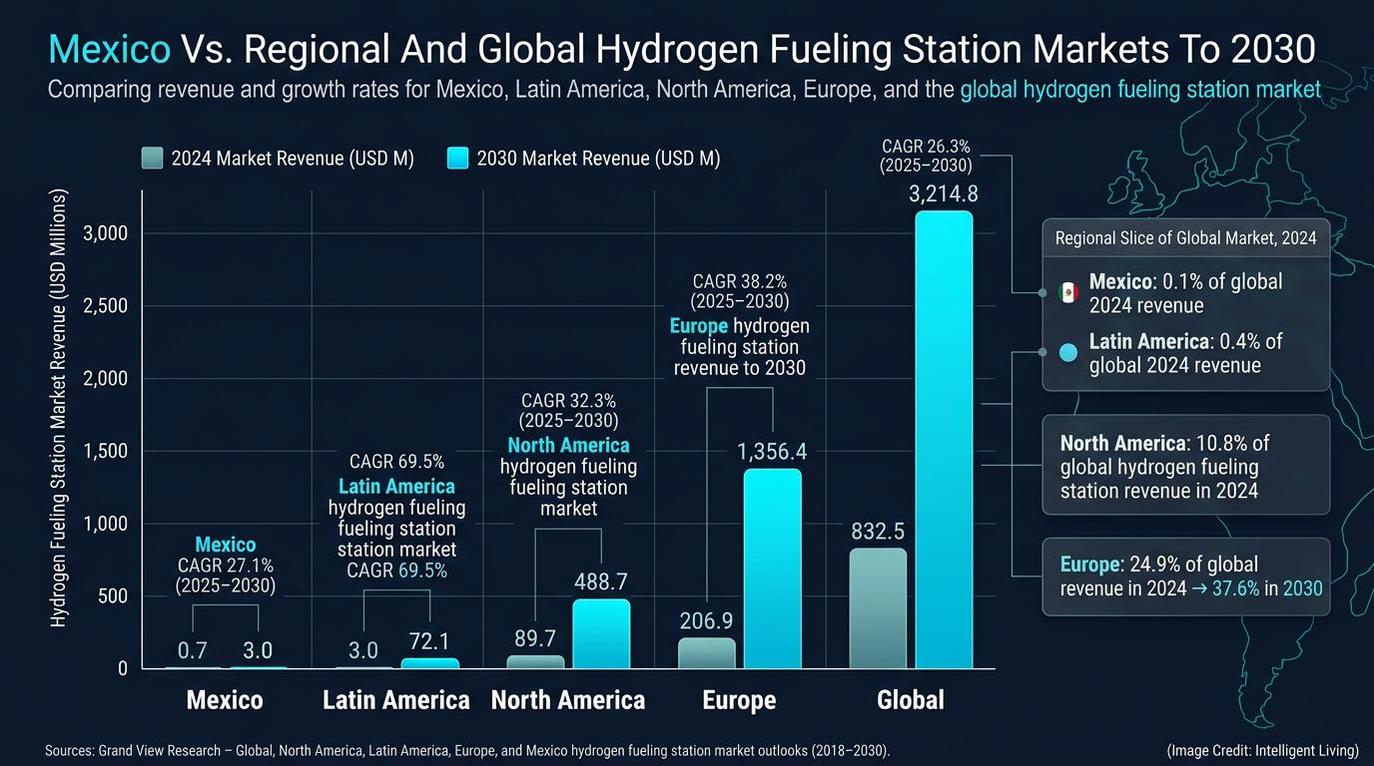

- The Mexico hydrogen fueling station market is projected to grow from $0.7 million in 2024 to $3.0 million by 2030, reflecting a 27.1 percent CAGR between 2025 and 2030.

- The Latin America hydrogen fueling station market is projected at $3.0 million in 2024 with a 69.5 percent CAGR through 2030.

- Northbound commercial crossings exceeding 7.4 million units annually.

- Port Laredo commerce currently accounts for critical cross-border trade value totaling $339.7 billion with 2.9 million inbound trucks.

These growth metrics underscore the urgency for strategic infrastructure deployment. Successful integration of these assets depends on how effectively they cluster around high-volume freight gateways.

Scenario modeling for heavy-duty hydrogen refueling projects approximately 14 H35 stations nationwide by 2030, with further acceleration expected in subsequent decades.

These projections derive from the following data sources:

- Mexico-Germany Energy Partnership hydrogen studies

- U.S. Bureau of Transportation Statistics reports

- Port Laredo trade data from the Texas Comptroller

Strategic Border Nodes: Why Freight Intensity Shapes Mexico’s Hydrogen Map

Why Hydrogen Freight Corridors Start at the Border, Not Everywhere

Hydrogen infrastructure mapping for the freight sector adheres to a strategic mandate: follow the trucks. Data from the U.S. Bureau of Transportation Statistics confirms that trucking dominates cross-border trade by dollar value. Annual goods flow totaling hundreds of billions of dollars centers on land ports like Laredo and Otay Mesa, representing the highest-volume freight gateways in North America.

California transborder commerce statistics show more than 7.4 million northbound commercial truck crossings annually, with Laredo exceeding 2.9 million inbound trucks and Otay Mesa surpassing 1 million. These high-volume gateways function as the structural arteries of North American trade rather than marginal transit routes.

Hydrogen refueling stations for heavy-duty trucks are expensive and must run at high utilization to make financial sense. Initial deployments gravitate toward border gates with consistent freight throughput to avoid the inefficiencies of a diluted national network. Real-time telematics-driven freight compliance mirrors this pattern, as infrastructure inevitably follows measurable traffic density.

The 2030 Reality Check: High CAGR, Tiny Base, and Why Nodes Beat a National Network

Grand View Research projects the Mexico hydrogen fueling station market to rise from $0.7 million in 2024 to $3.0 million by 2030, a 27.1 percent compound annual growth rate from a very small base. A small base with a high growth rate does not imply a dense nationwide station network by 2030; it implies a handful of targeted pilot deployments.

Latin America’s projected 69.5 percent CAGR for hydrogen fueling stations reflects similar base effects across the region. Early growth in new infrastructure markets typically appears steep because deployment begins near zero, which is why strategic node placement is more important than raw growth percentages.

The 2030 story centers on corridors rather than coverage, paralleling how green shipping arteries between ports focus on high-volume lanes rather than global blanket networks.

H35 Engineering Logistics: Optimizing the Fourteen-Station Decade

Hydrogen refueling for heavy-duty trucks typically relies on H35 stations, meaning 350 bar dispensing pressure. H35 standards define heavy-vehicle refueling requirements, distinguishing them from the 700-bar systems utilized by passenger cars. This pressure differential fundamentally alters compressor sizing, storage configurations, and the overall station footprint due to the massive fueling volumes required by heavy trucks.

Scenario modeling from the Mexico-Germany Energy Partnership indicates that Mexico could have roughly 14 H35 stations nationwide by 2030 before accelerating into the 2040s. Fourteen stations in a country the size of Mexico forces a clear conclusion. They must be placed where freight intensity is highest and where daily truck counts can support meaningful hydrogen throughput.

Throughput Dynamics and Amortization Scales

Heavy-duty station design prioritizes daily kilograms dispensed. Low-volume stations dispensing only a few hundred kilograms struggle to amortize the costs of compression, storage, and safety systems. High-volume corridor stations serving dozens of trucks daily dilute fixed capital costs across larger fuel quantities, validating the central logic of the corridor model.

Engineering constraints further reinforce the necessity of concentrated infrastructure. Hydrogen stations function as capital-intensive assets requiring specialized industrial components:

- High-pressure compressor systems

- Buffer storage tanks

- Advanced cooling systems

- Safety monitoring and reinforced foundations

U.S. Department of Energy data and National Renewable Energy Laboratory hydrogen station cost analyses demonstrate that station economics hinge on daily throughput. Low utilization rates dramatically increase the final cost per kilogram of dispensed fuel.

Network Continuity and Range Reliability

Modeling confirms that delivered hydrogen costs for heavy-duty fleets decrease as station size and utilization increase.

Operational success hinges on corridor continuity. Isolated stations cannot match the strategic utility provided by a synchronized chain of refueling points. This network structure ensures seamless round trips and eliminates range anxiety for fleet operators.

This parallels how China’s emerging hydrogen pipeline backbone concentrates early infrastructure along key industrial routes.

Northern Border Hydrogen Corridors: Texas and California Gates

Corridor Map 1: The Texas Gate (Monterrey → Nuevo Laredo ↔ Laredo)

Laredo is the most compelling early hydrogen freight node in North America’s southern corridor. The Texas Comptroller reports roughly $339.7 billion in trade flowing through Port Laredo, representing the majority share of Texas land port trade, with more than 2.9 million inbound trucks in 2023. That volume represents daily flows measured in thousands of trucks, not hundreds.

Manufacturing Nodes and Trade Volume Concentration

Existing freight density identifies the Monterrey–Nuevo Laredo–Laredo spine the premier candidate for early H35 deployment. Integrating hydrogen on this established route avoids the risk of creating new freight patterns. This approach allows stations to leverage existing traffic to achieve high daily throughput.

Binational Funding Mechanisms for Cross-Border Logistics

United States federal authorities have already initiated financing for large-scale hydrogen freight corridors. Recent funding announcements describe extensive build-outs throughout the Texas Triangle and Gulf Coast regions to support zero-emission logistics.

Federal Financing and Regional Hub Integration

The HyVelocity hydrogen hub serves as a prime example, having secured federal backing to initiate Phase 1 operations. These initiatives specifically target medium- and heavy-duty trucking to decarbonize regional haul routes.

Port Connectivity and Green Ammonia Export Hubs

At Port Houston, a $25 million grant-supported hydrogen refueling station project at Bayport signals that heavy-duty hydrogen is moving beyond theory into port infrastructure. The 240 megawatt green ammonia project on the Texas Gulf Coast illustrates how deep-water ports, pipeline networks, and skilled workforces give the region an edge as a hydrogen export hub. A Monterrey–Nuevo Laredo–Laredo corridor could plug directly into this ecosystem, allowing cross-border fleets to refuel in Mexico and the United States without rerouting or range compromise.

Corridor Map 2: The California Gate (Tijuana → Otay Mesa ↔ Southern California)

Otay Mesa surpassed 1 million inbound trucks in 2023, according to official California data. As a high-volume crossing near major logistics hubs in Southern California, it presents a second plausible hydrogen freight node.

Clean Energy Policy Alignment and ARCHES Hub Impact

Unlike the Texas corridor, which is anchored in trade value dominance, the California gate is anchored in proximity to dense port infrastructure, clean transportation policies, and an existing hydrogen ecosystem. California’s ARCHES hydrogen hub received an initial $30 million federal tranche to launch Phase 1 planning and development activities, increasing the likelihood that freight refueling capacity will expand around ports and logistics centers.

Binational Standards for Pilot Fleet Operations

While Southern California currently operates light-duty hydrogen infrastructure, the transition to heavy-duty refueling leverages established permitting frameworks and safety protocols. A Tijuana–Otay Mesa corridor would not require a nationwide Mexican build-out; it would require targeted binational alignment at one high-density crossing so pilot hydrogen fleets can operate along predictable drayage and regional haul routes.

Sonora Supply Gravity—Where Hydrogen Could Be Made to Feed Northern Freight

Northern Mexico’s hydrogen corridor logic also depends on supply. The Sonora Sustainable Energy Plan outlines ambitions around renewable energy and hydrogen development, supported by abundant solar resources in the region. High solar irradiation levels make large-scale electrolysis theoretically attractive if transmission, water access, and financing align.

International policy databases, such as the International Energy Agency, recognize the Sonora initiative as a definitive framework for scaling regional clean energy production. If large-scale hydrogen production emerges in Sonora, coastal or inland transport links could connect supply to northern freight nodes.

Global hubs co-locate abundant solar resources and industrial demand to turn remote energy into exportable molecules, as seen with large-scale green hydrogen complexes currently under development in Australia.

Water, Infrastructure, and Transport Considerations

Hydrogen logistics from production hubs to border terminals necessitate complex midstream engineering decisions. The water requirements for hydrogen production are significant, necessitating roughly nine liters per kilogram at the chemical level. Coastal production or integrated desalination could become part of long-term infrastructure planning.

Engineering choices for hydrogen transport between production sites and border terminals include:

- Compressed gas trucking

- Liquid hydrogen transport

- Conversion into ammonia carriers

Integrated ocean refinery designs further illustrate how industrial hubs pair fuel logistics with seawater intake and treatment processes.

Sonora serves as the gravitational center for supply, though it does not yet constitute immediate proof of corridor viability. Distribution networks determine freight feasibility. In regions where direct hydrogen transport is constrained, synthetic e-fuel production offers another route to move energy from remote sites to demand centers.

From Policy Pilots to Bankable Hydrogen Freight Infrastructure

Pilot-to-Policy: Mexico’s Hydrogen Rulebook is Being Written in Public

Infrastructure scales only when regulation stabilizes. Mexico’s Ministry of Energy, SENER, has published hydrogen guidelines that define hydrogen as an energy carrier. Such documents establish the foundation for a standardized permitting environment spanning stations, pipelines, and vehicle fleets.

Cross-border freight adds another layer of complexity. Hydrogen safety codes, vehicle certification standards, and fuel quality requirements must align on both sides of the border. Standardizing high-level guidelines into enforceable codes provides the definitive signal investors require to transition northern corridors from pilots to permanent assets.

Infrastructure Economics: What it Takes to Make a Heavy-Duty Station Pencil Out

Hydrogen stations for heavy-duty trucks require compression systems, high-pressure storage, and dispensers. These station-level economics are tightly coupled to midstream assets, such as the synchronized hydrogen supply chains currently linking producers and users in major European ports.

Capital Expenditure and Upstream Fuel Levers

Capital expenditure for a heavy-duty hydrogen station covers land, grid interconnection, and specialized high-pressure storage vessels. Upstream fuel prices remain a critical economic lever. Green hydrogen produced with renewable electricity currently costs between $3.50 and $6.00 per kilogram, though modular electrolysis technology aims to reduce production costs toward the $1 per kilogram range.

Operational Scaling: CAPEX Requirements and Fuel Price Levers

Utilization Benchmarks for Diesel Parity

Modeling confirms that utilization determines economic viability; high-throughput stations effectively dilute fixed costs across larger fuel volumes. Achieving long-haul trucking diesel parity depends heavily on delivered fuel prices, policy incentives, and station reliability.

What to Watch From 2026 to 2030: Signals That Corridors Are Becoming Infrastructure

- Confirmed station siting announcements near Nuevo Laredo or Otay Mesa.

- Public fleet purchase agreements for hydrogen heavy-duty trucks operating cross-border routes.

- Firm hydrogen offtake contracts between producers and logistics operators.

- Alignment between Mexican hydrogen regulations and U.S. safety and certification standards.

- Transparent uptime data for heavy-duty hydrogen stations.

Together, these signals indicate when cross-border hydrogen freight corridors are shifting from pilot projects to essential infrastructure.

Strategic Pathways for Northern Mexico’s Hydrogen Infrastructure

Establishing a functional hydrogen trade ecosystem demands deep regulatory harmonization between Mexico and the United States. Hardware alone cannot bridge the gap.

The initial fourteen stations will dictate the industrial map through 2030, identifying the regions prepared to dominate North American logistics. For investors and fleet operators, the strategy is clear: follow freight intensity, track policy milestones, and prepare for a border infrastructure powered by hydrogen.

Data-driven look at how Northern Mexico’s border freight spines could anchor the Mexico hydrogen fueling station market and heavy truck corridors by 2030.

Expert Insights on Mexico’s Hydrogen Freight Infrastructure

What is the projected count for the Mexico hydrogen fueling station market by 2030?

Scenario modeling identifies approximately 14 heavy-duty H35 stations nationwide by 2030, concentrating early infrastructure in high-volume northern corridors.

Why is H35 dispensing pressure the standard for heavy-duty hydrogen refueling?

H35 pressure levels (350 bar) are optimized for the massive onboard storage requirements of heavy trucks, allowing for faster throughput compared to passenger-focused 700 bar systems.

How do hydrogen-powered freight corridors impact cross-border trade value?

Cross-border trucking emissions reductions along the Laredo and Otay Mesa spines help shippers meet ESG mandates while maintaining the flow of billions in annual trade value.

Which regions in Northern Mexico lead in green hydrogen production potential?

The state of Sonora is the primary hub for production gravity, utilizing vast solar resources and the Sonora Sustainable Energy Plan to feed future northern fueling nodes.

What are the main economic bottlenecks for heavy-duty hydrogen stations?

Primary challenges include high initial capital expenditure for compression systems and the need for high daily utilization to lower the delivered cost per kilogram.

Reflecting global hydrogen demand statistics showing that adoption remains in the early stages, while current hydrogen vehicle maturity indicates that adoption remains concentrated in specific Asian and North American markets.

{kind=link}