Paying your bills shouldn’t feel like a high-stakes guessing game every time the first of the month rolls around or your paycheck hits your account late on a Friday afternoon. Yet plenty of households run into the same sour surprise: a debit card declines, an overdraft fee appears, and no one is quite sure which transaction triggered it. These moments are exactly why the Consumer Financial Protection Bureau’s Personal Financial Data Rights rule—often called open banking in the United States—is so vital.

Section 1033 sets out to put you back in the driver’s seat. By making your transaction history portable, you can easily compare different data providers, dodge those annoying bank fees, and move your money to a new institution without the usual stress. While legal timelines are shifting, the CFPB’s current enforcement posture regarding Section 1033 summarizes the current enforcement posture and provides specific dates for stayed compliance. Even with policy changes unfolding, the core principle remains: your financial data belongs to you, not the institution.

Gaining a clear view of consumer-directed data access helps you reduce fee risk and makes switching banks far less stressful. When you authorize third parties to see your transaction history on your terms, you gain the leverage needed to find better rates and more transparent services.

Open Banking Quick Facts: Understanding Section 1033 and Your Financial Data Rights

Open banking and personal financial data rights are often discussed like they are “future tech,” but the underlying behavior already shows up whenever a budgeting tool links to a checking account or a lender verifies cash flow. The rule matters because it tries to make those connections more standardized, more controllable, and less dependent on password sharing.

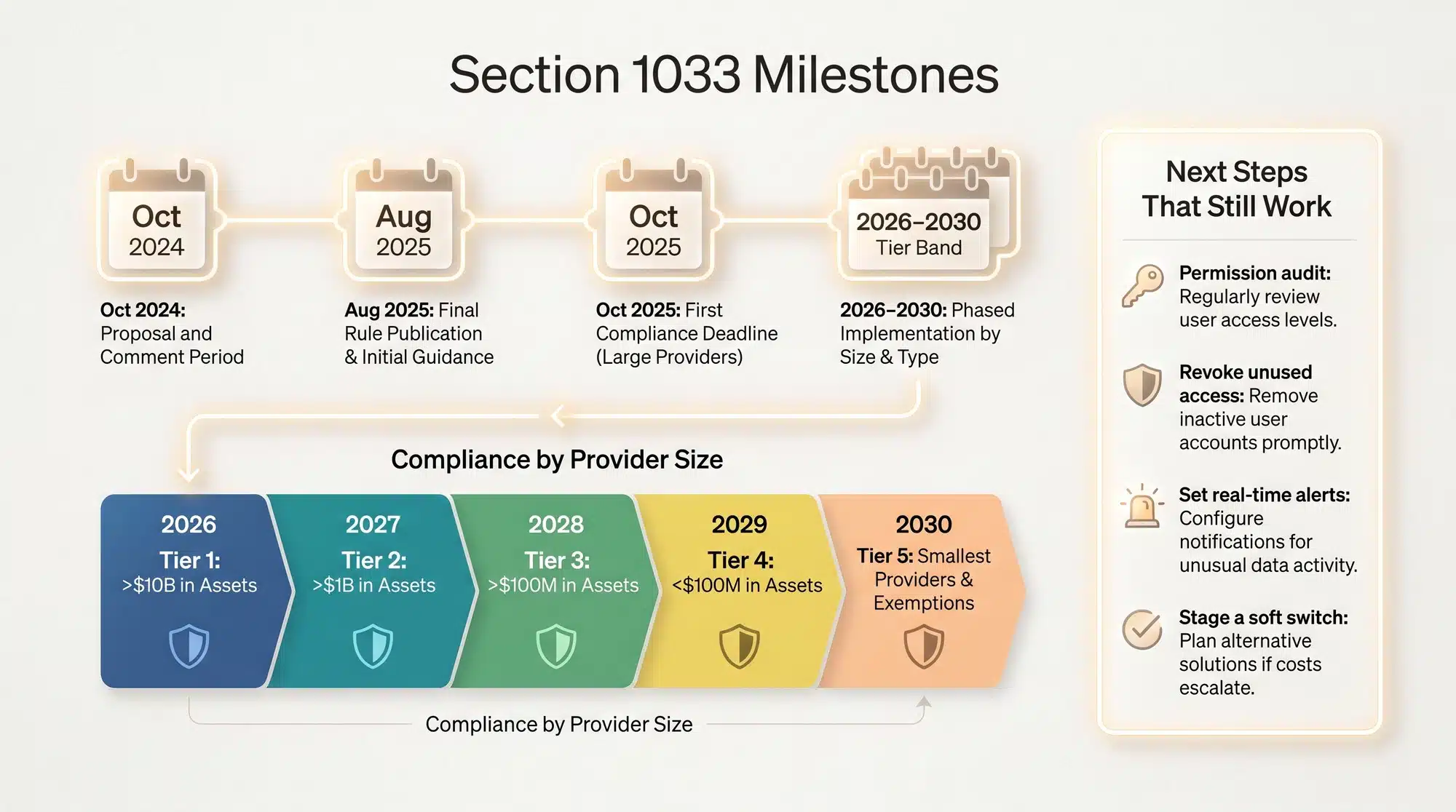

- The CFPB finalized the Personal Financial Data Rights rule on October 22, 2024, with a final announcement detailing consumer-directed access meant to support competition and privacy.

- A federal court later blocked enforcement while reconsideration proceeds, and the official court order staying Section 1033 enforcement remains the public record of that pause.

- The rule’s covered-data idea includes everyday essentials people actually use, like transactions, balances, and account terms.

- The regulatory definitions found in 12 CFR Part 1033 provide essential clarity on how data providers and authorized third parties must interact to protect your privacy.

- The CFPB’s research into total bank overdraft and NSF revenue reveals that 2019 charges reached roughly $15.47 billion, explaining why fee design remains a high-stakes issue.

- Detailed findings regarding consumer experiences with overdraft timing describe posting delays and late alerts that trigger fees even when money appears available.

These facts show that the conversation goes far beyond just moving data. It’s really about knowing exactly what fees you’re paying, making it easier to switch banks when you find a better deal, and keeping track of who can still see your private activity after you stop using an app.

Open Banking Fundamentals: Plain-English Guide to Cutting Fees and Switching Banks

Section 1033 Explained: What Open Banking and Data Portability Mean for You

Personal Financial Data Rights in One Sentence

Open banking isn’t a mechanism for banks to sell personal data; rather, it empowers U.S. consumers to access and share their financial history with any authorized company they choose.

Section 1033 and Consumer-Directed Data Access

The logic behind Section 1033 is straightforward: if your checking account creates a history of your spending and fees, you should be the one who decides where that information goes next. The CFPB’s overview of personal financial data rights explains this basic obligation in everyday language, including the push for standardized formats.

A useful way to picture it is keys. A bank account produces data, and a consumer decides who gets a copy and for how long. That might be a budgeting app used during a tight season, a lender checking cash flow for an offer, or a payments service that makes bill handling smoother.

APIs, Screen Scraping, and Why the Connection Method Matters

The biggest technical detail is how the connection happens. The CRS analysis of secure open banking frameworks notes that application programming interfaces (APIs) allow systems to share data without compromising login credentials. In contrast, screen scraping often means sharing a username and password so an app can copy information from what appears on the screen. That difference matters because password sharing can expand risk if an account or device is compromised.

Consider a typical scenario where you track grocery spending during a high-inflation month and then stop using the tool as your routine stabilizes.

A robust permission model allows you to revoke access immediately when the app’s utility ends. This prevents ‘zombie’ connections from silently accessing your bank balance in the background long after you’ve moved on.

Why Fees and Switching are the Big Real-World Stakes

The Timing Gap that Triggers Overdrafts

Data portability may sound abstract until it touches a bank account balance. Overdraft and non-sufficient funds fees historically generate billions in revenue, typically penalizing households during periods of extreme financial strain.

Real-world timing traps are often hidden behind those big bank revenue numbers, catching households off guard when processing delays create a mismatch between your app balance and your actual available cash.

Consider these common scenarios where timing gaps create fee risk:

- A utility bill posts to your account before your direct deposit paycheck fully clears.

- A grocery purchase made on a Sunday doesn’t settle until Wednesday afternoon.

- Subscription renewals trigger overnight while your bank’s systems are updating.

The CFPB’s qualitative findings highlight widespread confusion regarding these transaction windows. Even when you believe money is available, these specific posting gaps can trigger unexpected non-sufficient funds (NSF) fees.

Three Overdraft Choices that Change the Outcome

For people who keep getting clipped by fees, the CFPB’s tools for avoiding bank overdraft charges outline three practical paths that often matter more than luck: opting out of debit and ATM overdrafts, linking a savings account, or using a line of credit. The value of these options is not just the fee itself; it is the predictability they add when a month is already packed with bills.

Money habits get easier when there is a plan that fits the calendar, and a structured plan for reaching financial wellness can make it simpler to visualize where buffers and bill timing actually belong.

Why Easier Switching to Pressures Fee Design

When financial data is easier to access and compare, switching to an account with lower fees or clearer alerts becomes more realistic. The CFPB described the rule as a way to help families comparison shop and move accounts if a better option exists. While enforcement timelines are uncertain, the real-world logic is still easy to understand: if switching becomes easier, providers have stronger incentives to compete on fees and clarity.

A common trigger is a job change that forces a direct deposit update. If moving recurring payments and checking account habits feels simple, staying stuck in a high-fee account feels less inevitable. If moving money systems feels like moving houses, inertia wins.

Fees and switching are where policy language meets lived experience.

Immediate Actions: How to Manage Your Financial Data Control Today

Legal timelines may shift, but personal habits can change immediately. The goal is not to memorize regulation language; it is to treat financial data access like something that can be granted, limited, and cleaned up.

Run a 15-Minute Permission Audit

Try setting a timer for fifteen minutes. Head over to your bank’s security settings or your account-linking dashboard to see exactly which third-party apps still have a green light to view your transactions.

According to the security principle of least privilege, you should only grant the minimum access needed for the job and remove anything that no longer serves a purpose. Applied to personal finance, that means unused apps should not retain access to live transaction data.

A quick audit can be as simple as three checks: whether the app is still used, whether it needs transaction history or only balances, and whether there is a clear revocation switch.

A very real modern scenario is a finance app that shuts down with deadlines for exporting records and turning off bank access. A comprehensive checklist for closing financial app accounts captures how quickly a convenient connection can become a loose end if it is not closed out deliberately.

Understand Disconnect Versus Delete

Stopping future sharing and deleting stored data are not always the same action. In many account-linking systems, severing your bank connections with a third-party app means new data stops flowing, even though older records might still exist elsewhere.

Deletion is a different step. Some systems describe deletion as removing the linked institution record itself, which is similar to the process for purging your records from a central data portal. This is why it helps to treat disconnecting and deleting as separate checklist items.

Maintain a strategic distinction between these two actions: while disconnecting an account terminates future data sharing, only a formal deletion request removes the historical records an app has already harvested.

Users who uninstall budgeting apps without revoking access often incorrectly assume all data sharing has ceased. In reality, a data connection can still exist until it is explicitly removed.

Build a Bill Calendar that Exposes Timing Gaps

The CFPB’s overdraft research highlights confusion around posting times. Mapping out your paydays alongside your rent, utilities, and subscriptions can reveal those dangerous fee-risk weeks long before they arrive. This simple calendar view clears up the confusion around posting times that the CFPB frequently warns about.

A 90-day cash flow management strategy treats those weeks as the main event, ensuring you stay ahead of potential shortfalls. Even a handwritten calendar on the refrigerator can show that three automatic payments hit before a paycheck on certain months.

One extra step adds clarity fast: flag days where a paycheck is pending but not settled, since that is where posting delays can collide with autopays.

That visibility can guide adjustments such as moving payment dates or keeping a buffer during known tight windows.

These steps do not require a finalized regulation. They rely on awareness and deliberate control.

Practical Switching and Fee Defense: How to Eliminate Overdraft Fees and Soft Switch Banks

Step-by-Step Soft Switching: Move Your Money without the Stress

You don’t have to cut ties with your old bank overnight just to find a better deal. Since your paycheck and bills are so intertwined, moving your money in stages makes the transition much smoother.

A practical approach known as soft switching allows you to test a new bank while keeping your original account active. This method for managing two active bank accounts is a proven way to avoid missed payments while you evaluate new fee structures and alert speed.

Step 1: Open and Fund the New Account

Deposit a modest amount and test basic functions. Confirm that debit card transactions clear as expected and that mobile alerts work.

One small but telling test is whether low-balance alerts arrive quickly enough to be useful, not hours after a purchase.

Step 2: Move Direct Deposit First

Updating your payroll information ensures your income remains stable throughout the transition. Once you verify that two pay cycles have settled in your new account without issue, you can safely proceed to phase out your old institution.

If paychecks arrive at different times depending on weekends or holidays, note those patterns during the overlap period so bill timing stays realistic.

Step 3: Transfer Recurring Bills in Waves

You can minimize disruption by prioritizing your most critical, time-sensitive obligations first—such as rent, mortgage payments, or childcare—before moving on to smaller recurring subscriptions.

During this transition, a small cushion in the old account can prevent accidental overdrafts. A two-paycheck overlap often provides enough breathing room to close the old account without anxiety.

Choosing a new bank also means choosing stability, and the fundamentals of FDIC insurance coverage clarify what protection actually covers when you spread funds across multiple institutions.

If open banking frameworks eventually simplify data portability, this process may become more automated. For now, structured steps reduce chaos.

Three Proactive Controls to Stop Surprise Bank Fees

1. Activate Real-Time Low-Balance Alerts

Many banks allow low-balance and transaction alerts through text or app notifications. The CFPB’s advice on stopping debit card overdraft fees highlights alerts and bill timing as essential protections, especially when settlement delays are common.

Alerts work best when they are specific, like a low-balance threshold that matches a household’s bill schedule, not a generic warning that arrives too late.

2. Maintain a Strategic Cash Buffer to Absorb Timing Gaps

Keeping even a tiny cash cushion in your account acts like a shock absorber for timing gaps. If you’re living on a tight budget, that small buffer can be the only thing standing between a quick dip and a painful cascade of fees.

A buffer does not need to be huge to be effective; it just needs to be consistent and protected from routine spending.

3. Compare Fee Structures and Search for Better Account Terms

Clearer access to account terms and transaction history makes comparison shopping much more concrete. You can now evaluate banks based on specific features that protect your wallet.

Focus on finding accounts that offer:

- Generous grace periods for deposits.

- Significantly lower overdraft fees.

- Entirely no-fee banking structures.

If you struggle to stay consistent with manual tracking, simple systems that run quietly in the background are usually more effective. Learning how automated habits simplify your financial life can turn your alerts and transfers into a background process that protects you without daily effort.

Open Finance Safety: Protecting Your Privacy, Consent, and Financial Data Connections

Safety and Trust: How to Share Data Without Regret

What Privacy Rules Cover and What they Do Not

Financial privacy in the United States has long been shaped by the Gramm-Leach-Bliley Act, which requires financial institutions to explain how they share nonpublic personal information. The FTC’s regulations regarding consumer financial privacy explain why disclosures matter and why consumers should care about who can access financial data.

It is easy to skip past those lengthy privacy disclosures, but they contain the fine print on how your data travels. These documents explain if you can opt-out of sharing, which affiliates see your information, and the specific safeguards protecting your records.

Consent Screens that Signal Risk

When authorizing a third-party app, ensure the consent screen explicitly details the data categories being accessed and the exact revocation procedure. A lack of transparency in the onboarding flow is a clear indicator of potential privacy risk.

A good consent flow is specific about scope, like transactions for a date range, and it is specific about control, like a visible revocation switch.

Revocation should be straightforward. Deletion should be possible when requested. Trust grows when control is visible.

Scams and Device Security that Undermine Consent

Most financial losses result from avoidable user errors rather than sophisticated cyberattacks or Hollywood-style breaches. Learning to spot fake spam text messages from scammers reduces the odds of handing over credentials to a fraudulent source.

Your phone security is now your money security. Since almost all modern banking happens on a mobile device, a lost or tracked phone provides a direct window into your entire financial life. Your best habits for securing your mobile banking device tend to be unglamorous, like updates, strong authentication, and refusing unknown links.

Data Minimization as a Money Habit

The safest data is the data that is never collected in the first place. Essential safeguards for protecting your online financial data reinforce the theme of least privilege: share less, keep control, and clean up old permissions.

A simple rule keeps it practical: if an app does not need full transaction history to do its job, avoid granting it.

Small Box for Teams: Build Consent that Humans Understand

Plain-Language Permissions and Clean Revocation

Developers and product teams play a central role in whether open banking builds trust or erodes it.

Clear consent screens written in everyday language reduce accidental permissions. Simple dashboards that list connected accounts and provide one-click revocation make control meaningful rather than symbolic.

Standardization that Keeps Control Intact

Industry standards work has treated consent as part of the product, not a footnote. Standardized design targets consistency. This ensures you don’t have to learn a new ‘permission language’ every time you decide to link a new financial service. The industry standards for API consent and revocation describe why transparency must stay in sync across all parties.

A practical design target is consistency, so users do not have to learn a new permission language every time they connect a new service.

Data Flows People Can Actually Understand

Using transparent data flows that improve user trust treats consent as a process people can understand, not a wall of legal text. When permission screens show what is collected, why it is needed, and how to turn it off, users stop feeling trapped.

When consent flows are readable and reversible, consumer confidence strengthens.

Rule Updates and Action Plan: The Current Section 1033 Timeline and Your Next Steps

Reality Check: What’s Happening with the Timeline

What Stayed and Why Timelines Matter

The CFPB finalized the Personal Financial Data Rights rule in October 2024. In late October 2025, a federal court blocked enforcement while reconsideration proceeds.

That does not erase the core idea, but it does mean people should treat compliance dates and rollout assumptions as moving pieces.

What the Reconsideration Focus Suggests

The Bureau’s specific reconsideration queries focus on representatives, fees, and the threat picture for security and privacy, which signals the kinds of implementation details that could still change.

9 Ways to Use Personal Financial Data Rights Principles to Improve Your Money Life

You don’t need expert technical knowledge to master your money; financial empowerment begins with consistent habits that harden your digital privacy. While the CFPB navigates the legal landscape of Section 1033, you can implement these strategies to harden your financial defenses.

Use this checklist to optimize your data rights and reduce fee exposure:

- Run a quarterly permission audit to see who has your data.

- Revoke access for any unused or forgotten financial apps.

- Treat disconnecting an account and deleting data as two separate security steps.

- Activate real-time low-balance and transaction alerts immediately.

- Create a bill calendar to expose high-risk timing gaps.

- Maintain a modest cash buffer during any account transitions.

- Use a soft switching strategy before closing an old bank account.

- Perform an annual review of your bank’s fee schedule.

- Treat your financial data like keys that you can hand out or take back.

These nine steps shift the power back to you. By treating your transaction history as a valuable asset, you reduce the likelihood of being caught by a ‘dark pattern’ or an unnecessary fee.

If only one step happens this week, make it the permission audit, because it shortens the list of places where data can leak or be misunderstood. If two steps happen, add a bill calendar, since timing clarity is often the difference between a tight month and a fee month.

Maximize Your Savings: Take Control of Your Financial Data and Fee Risk Today

Personal financial data rights and open banking are deeply practical tools for your wallet. Having real-time control over your transaction history and clarity around non-sufficient funds (NSF) fees makes financial stability much easier to reach. Even as legal timelines move, adopting habits like a quarterly permission audit and alert activation can lower your costs immediately.

The signals that help you make better financial choices usually come down to plain things: clear fees, clear controls, and clear accountability when something goes wrong. By practicing data minimization and monitoring your revocation lifecycle, you ensure your information only works for you. Your money data tells your story; when it is portable and understandable, you finally gain leverage over your banking future.

Common Questions About CFPB Open Banking and Personal Financial Data Rights

Is CFPB Open Banking on hold?

A federal court recently blocked enforcement while the rule is reconsidered. While the statutory authority remains, the exact rollout timeline for these data rights is currently in flux.

What data can be shared under Section 1033?

You can share your transaction history, account balances, and specific account terms. This allows authorized third-party apps to help you budget or find better financial products.

Does revoking access delete my bank data?

Revoking access stops new data from flowing to an app. To remove records already stored by that company, you usually need to follow a separate deletion process within their specific portal.

How do I reduce bank overdraft fees quickly?

Set up real-time low-balance alerts, map your bill timing to your paydays, and maintain a small buffer in your checking account to absorb processing delays.

Is it safe to link my bank account to an app?

Safety depends on the connection method. It is best to use apps that connect via secure APIs rather than password sharing (screen scraping) and offer clear permission dashboards.

What can you do if an overdraft fee feels wrong?

The instructions for disputing an overdraft fee from the CFPB explain opt-in rules in plain terms, including when a bank cannot charge a fee without your explicit consent.

When a problem does not resolve through normal customer service, the process for filing a consumer banking complaint can route your concern directly to the company for a response and create a paper trail for follow-up.

{kind=link}